You can use a home equity loan for many purposes. You can use the money to consolidate debt, pay off high-interest debt or invest in savings accounts. However, the loan should not be used to accumulate additional debt. Before you can set a budget, it is essential to know your limits.

Home improvement

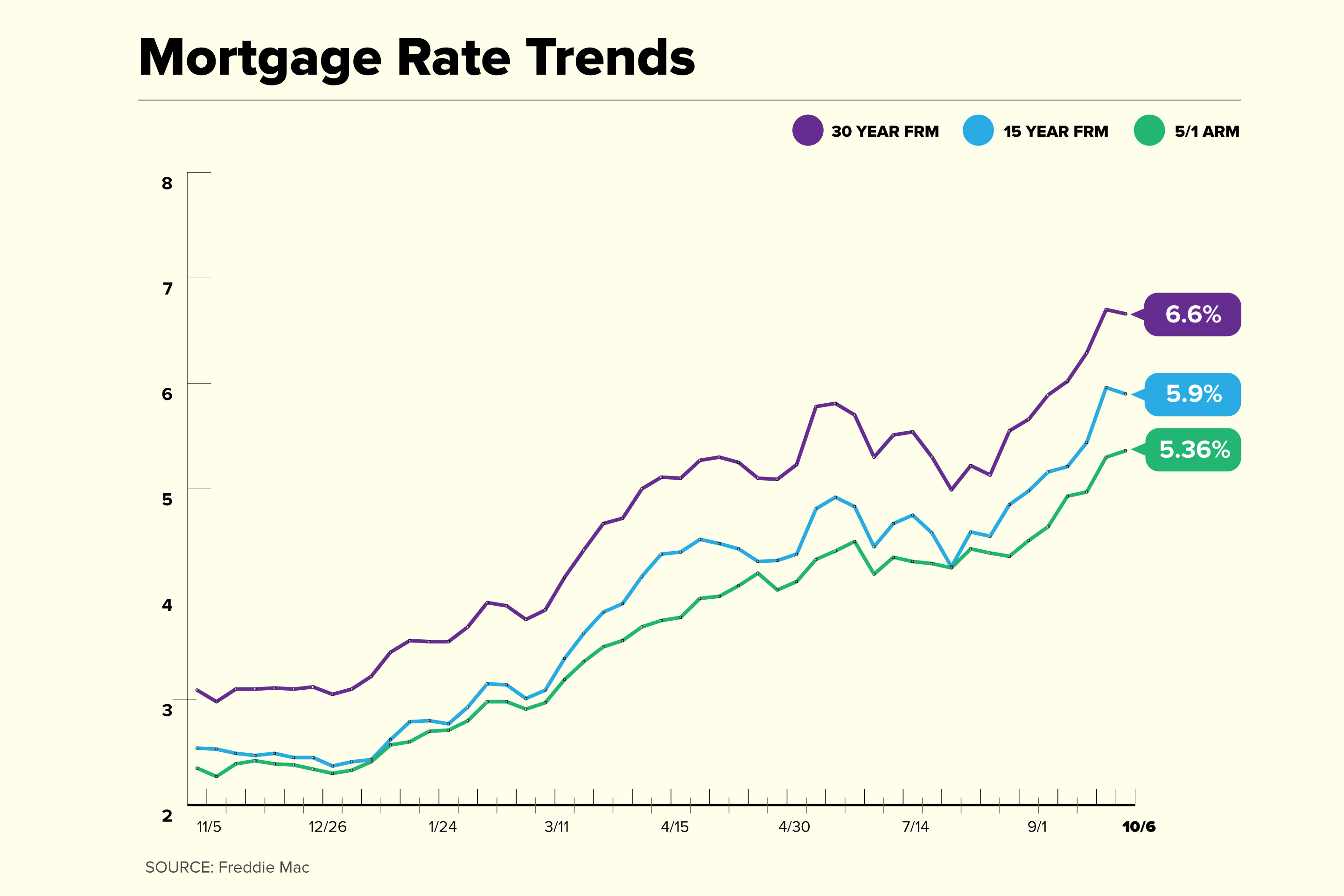

A home equity loan can be used to fund many things, including home renovations. Home improvements can be costly, so home equity can be a great resource to help you fund them. A home equity loan has a low interest rate, which is one of its main benefits. As of January 2022, the average rate for home equity loans was 5.96%.

Home improvement can be a huge project, but the process does not need to be permanent. The money can be used for home improvements or furniture upgrades. Homeowners can also use the money for home improvements like adding a bathroom or replacing old flooring. Home equity loans offer homeowners the opportunity to make home improvements and continue living in their homes. Home equity loans cannot be used for construction because they require a separate construction loan.

Consolidation

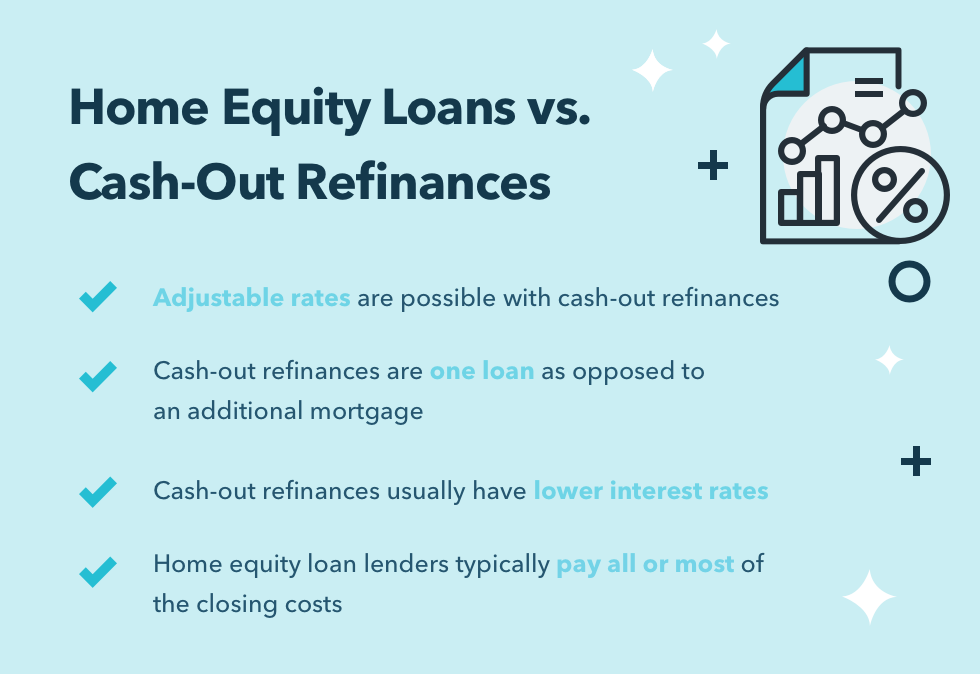

A home equity loan could be a viable option to consolidate debt. You can use your home as collateral to get a lower interest, which can be a benefit when budgeting. Home equity can be used as collateral. If you fail to pay your mortgage payments, your home could be foreclosed or forfeited. In addition, you may be required to pay extra costs such as home appraisals and closing costs, and the application process can take up to 30 days.

Consolidating debt with a home equity loans can lower your interest rate, make repayments easier, and reduce your monthly payments. It is important to remember that your home may be in danger of foreclosure. Secured loans come with lower rates, simpler terms, and will not affect your credit score. You have other options, such as personal loans and credit cards, for consolidating debt.

Venture capital

If you're planning to start a new business, home equity loans may be a good option. While most banks are hesitant to fund new businesses, a home equity loan can provide the cash you need to get your business up and running. Since there are no specific rules about using home equity for business purposes, home equity loans can be a great way to fund your new business.

You might believe home equity is the best way of financing a new business. But, it isn't always the best. Although home equity can be a good option, you should know that home equity loans also have their risks and drawbacks.

How to pay off high-interest loans

A home-equity loan could be the solution to your debt problems if you have lots of it. You should consider the cost of such a loan. The interest rates on these loans can be lower than those on other debts, but the closing costs and other fees can outweigh the savings you can achieve.

You can borrow home equity to pay for renovations or repairs to your house. However, you should know that it can affect your credit score if you don't use them properly. You should be aware that home equity loans are subject to long repayment terms. You could end up in debt if you fail to repay the loan amount on time.

FAQ

What are the 3 most important considerations when buying a property?

When buying any type or home, the three most important factors are price, location, and size. Location is the location you choose to live. Price refers how much you're willing or able to pay to purchase the property. Size refers the area you need.

Do I need a mortgage broker?

If you are looking for a competitive rate, consider using a mortgage broker. Brokers can negotiate deals for you with multiple lenders. Some brokers earn a commission from the lender. Before you sign up for a broker, make sure to check all fees.

What is a Reverse Mortgage?

Reverse mortgages are a way to borrow funds from your home, without having any equity. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types of reverse mortgages: the government-insured FHA and the conventional. A conventional reverse mortgage requires that you repay the entire amount borrowed, plus an origination fee. If you choose FHA insurance, the repayment is covered by the federal government.

How do I calculate my interest rate?

Market conditions can affect how interest rates change each day. In the last week, the average interest rate was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. For example, if you finance $200,000 over 20 years at 5% per year, your interest rate is 0.05 x 20 1%, which equals ten basis points.

How long does it take for my house to be sold?

It depends on many factors including the condition and number of homes similar to yours that are currently for sale, the overall demand in your local area for homes, the housing market conditions, the local housing market, and others. It takes anywhere from 7 days to 90 days or longer, depending on these factors.

What are the benefits associated with a fixed mortgage rate?

Fixed-rate mortgages allow you to lock in the interest rate throughout the loan's term. This means that you won't have to worry about rising rates. Fixed-rate loans have lower monthly payments, because they are locked in for a specific term.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to purchase a mobile home

Mobile homes are homes built on wheels that can be towed behind vehicles. Mobile homes were popularized by soldiers who had lost the home they loved during World War II. People today also choose to live outside the city with mobile homes. Mobile homes come in many styles and sizes. Some are small, while others are large enough to hold several families. There are some even made just for pets.

There are two main types for mobile homes. The first type is produced in factories and assembled by workers piece by piece. This takes place before the customer is delivered. You could also make your own mobile home. Decide the size and features you require. Next, make sure you have all the necessary materials to build your home. Finally, you'll need to get permits to build your new home.

There are three things to keep in mind if you're looking to buy a mobile home. Because you won't always be able to access a garage, you might consider choosing a model with more space. Second, if you're planning to move into your house immediately, you might want to consider a model with a larger living area. Third, you'll probably want to check the condition of the trailer itself. It could lead to problems in the future if any of the frames is damaged.

Before buying a mobile home, you should know how much you can spend. It is crucial to compare prices between various models and manufacturers. It is important to inspect the condition of trailers. Although many dealerships offer financing options, interest rates will vary depending on the lender.

It is possible to rent a mobile house instead of buying one. Renting allows you the opportunity to test drive a model before making a purchase. However, renting isn't cheap. The average renter pays around $300 per monthly.