Home equity can be used to determine the value of your house. You can use an online value estimator tool to determine how much equity you have in your property. The most recent property appraisal can be used to calculate your mortgage balance. To obtain an exact estimate of your property equity, you can call your mortgage lender to request an official appraisal.

Get a home equity mortgage

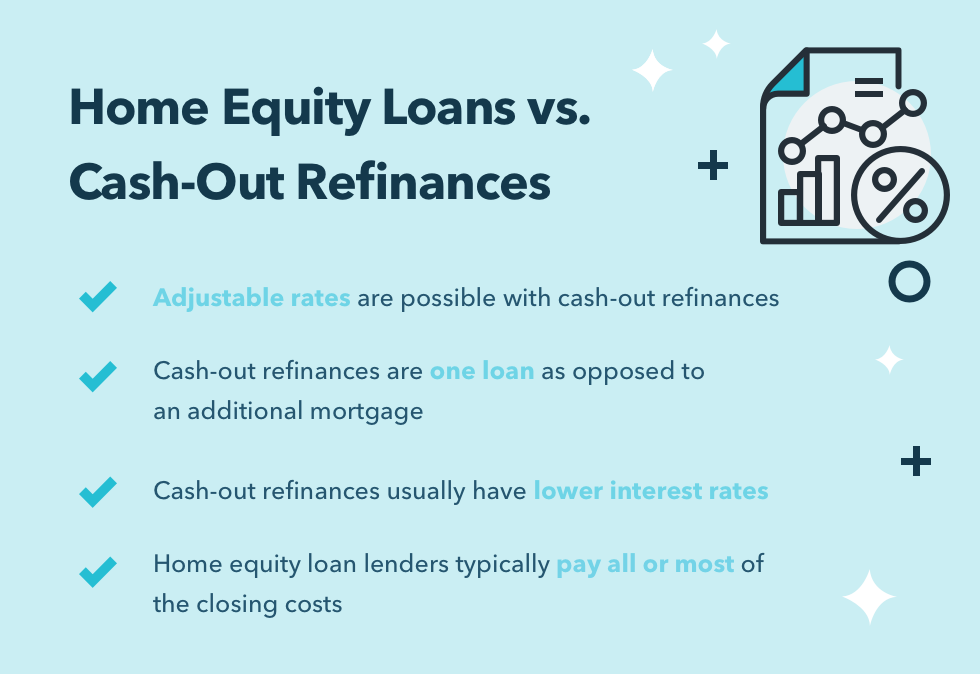

If you have equity in your home, getting a home equity loan is an excellent way to pay off debt. Compared to a traditional loan, a home equity loan allows you to pay off your debt with one large lump sum. A fixed interest rate will apply for the entire loan term, which will lock you into monthly payments that will not change. This type loan can also be combined to a cash-out mortgage.

It is important to calculate your equity. Most lenders will allow you to borrow up to 80% of the value of your home. To be eligible, you must have at minimum 20% equity in your house. Even if your credit score is not exceptional, you might still be eligible to receive a home equity mortgage with less equity.

Building equity

A homeowner's goal is to create home equity. You can use it to improve the value of your house when you sell it. To help build your equity, you can apply for home equity loans and credit lines. A large down payment, or paying more towards your mortgage are some easy ways you can increase your equity.

Energy-efficient appliances are a great way to increase the home's worth. To boost your home's value, double-paned Windows and LED Lighting can be installed. Smart thermostats or solar panels are also options. A fully finished basement or modern bathroom will help increase the property's market value.

Refinance your loan to increase your equity. You can refinance your loan to get a lower rate and a shorter term. This will allow you to pay more towards the principal. Your equity will increase as time passes and you start paying more money into the principal.

How to take equity out of your home

There are several reasons you shouldn't take equity out of your house. It could place you in an even worse situation than what you are currently in. If you fail to make your monthly payments, your home might be foreclosed. A foreclosure will remain on your credit report for seven year. If you do not have enough cash to repay the loan, a judgment of deficiency will be issued against the borrower. This will enable your lender to garnish wages, levy bank accounts, or place a lien against your property. Your home's value will drop if you don't make your payments on time.

If you are considering taking equity out of your home, it is important to know the value of your home so you can make an informed decision. It is also important to create a plan before you take any equity out. It's important that you only use the money for things that will pay off in the long term. You may be looking to consolidate debt, improve the value of your home, or go on a vacation.

FAQ

What are the most important aspects of buying a house?

The three most important factors when buying any type of home are location, price, and size. It refers specifically to where you wish to live. Price refers the amount that you are willing and able to pay for the property. Size refers the area you need.

What's the time frame to get a loan approved?

It is dependent on many factors, such as your credit score and income level. It generally takes about 30 days to get your mortgage approved.

Should I rent or own a condo?

Renting could be a good choice if you intend to rent your condo for a shorter period. Renting allows you to avoid paying maintenance fees and other monthly charges. A condo purchase gives you full ownership of the unit. You have the freedom to use the space however you like.

How do I calculate my interest rates?

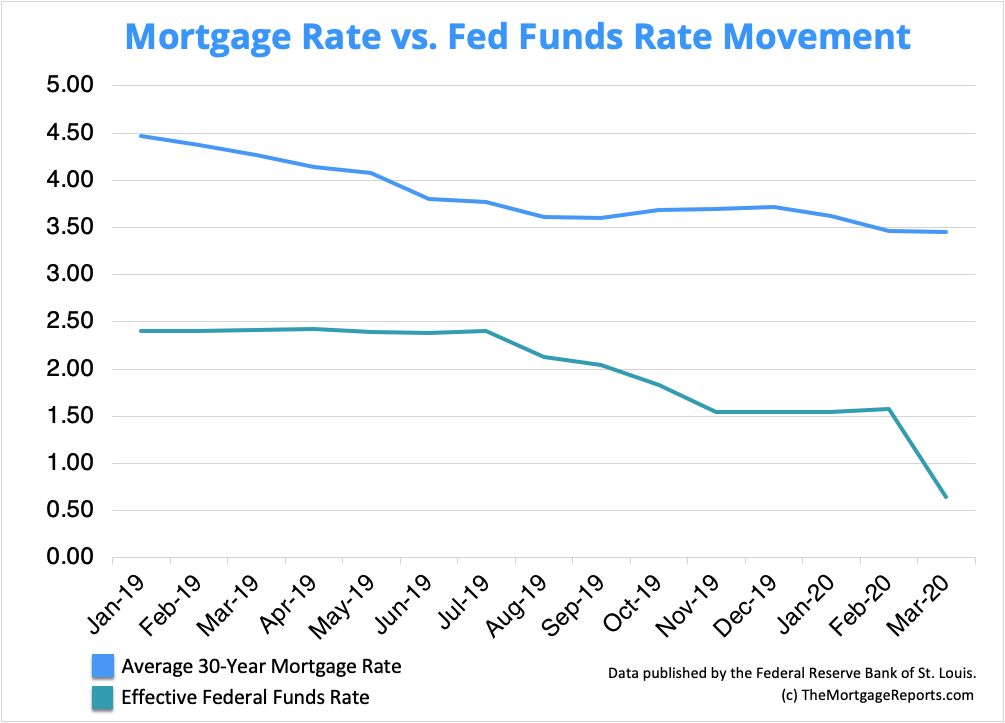

Market conditions affect the rate of interest. The average interest rate during the last week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. For example, if $200,000 is borrowed over 20 years at 5%/year, the interest rate will be 0.05x20 1%. That's ten basis points.

Is it possible fast to sell your house?

You may be able to sell your house quickly if you intend to move out of the current residence in the next few weeks. However, there are some things you need to keep in mind before doing so. First, you need to find a buyer and negotiate a contract. Second, prepare the house for sale. Third, it is important to market your property. Lastly, you must accept any offers you receive.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to Find Real Estate Agents

The real estate agent plays a crucial role in the market. They can sell properties and homes as well as provide property management and legal advice. Experience in the field, knowledge about your area and great communication skills are all necessary for a top-rated real estate agent. Look online reviews to find qualified professionals and ask family members for recommendations. It may also make sense to hire a local realtor that specializes in your particular needs.

Realtors work with residential property sellers and buyers. A realtor's job is to help clients buy or sell their homes. As well as helping clients find the perfect home, realtors can also negotiate contracts, manage inspections and coordinate closing costs. Most realtors charge commission fees based on property sale price. Unless the transaction closes, however, some realtors charge no fee.

The National Association of Realtors(r), (NAR), has several types of licensed realtors. To become a member of NAR, licensed realtors must pass a test. A course must be completed and a test taken to become certified realtors. NAR designates accredited realtors as professionals who meet specific standards.